Over the last few years, and particularly in 2020, M&A activity in the games industry has headed into overdrive, with multi-billion dollar acquisitions, key investments, and partnerships. Headline deals include Zynga’s $1.8 billion acquisition of Peak Games, as well as its purchases of Rollic Games, Small Giant Games, and Gram Games, while Scopely has been busy acquiring the likes of FoxNext Games and Digit Game Studios. Then there are major partnerships, such as Activision and Tencent’s collaboration on Call of Duty: Mobile, which generated approximately $480 million worldwide from player spending in its first year on the App Store and Google Play. This analysis looks at how these deals—and many others—have reshaped market share in the mobile gaming space.

Utilizing Sensor Tower’s Game Taxonomy and Store Intelligence platform, we analyzed several of the top genres by player spending in the United States throughout Q1 to Q3 2020 to look at which publishers are controlling the largest market share in the space. From this data, we can see how a publisher’s portfolio of titles is performing in a particular category, while also identifying how new launches and M&A activity have impacted the market.

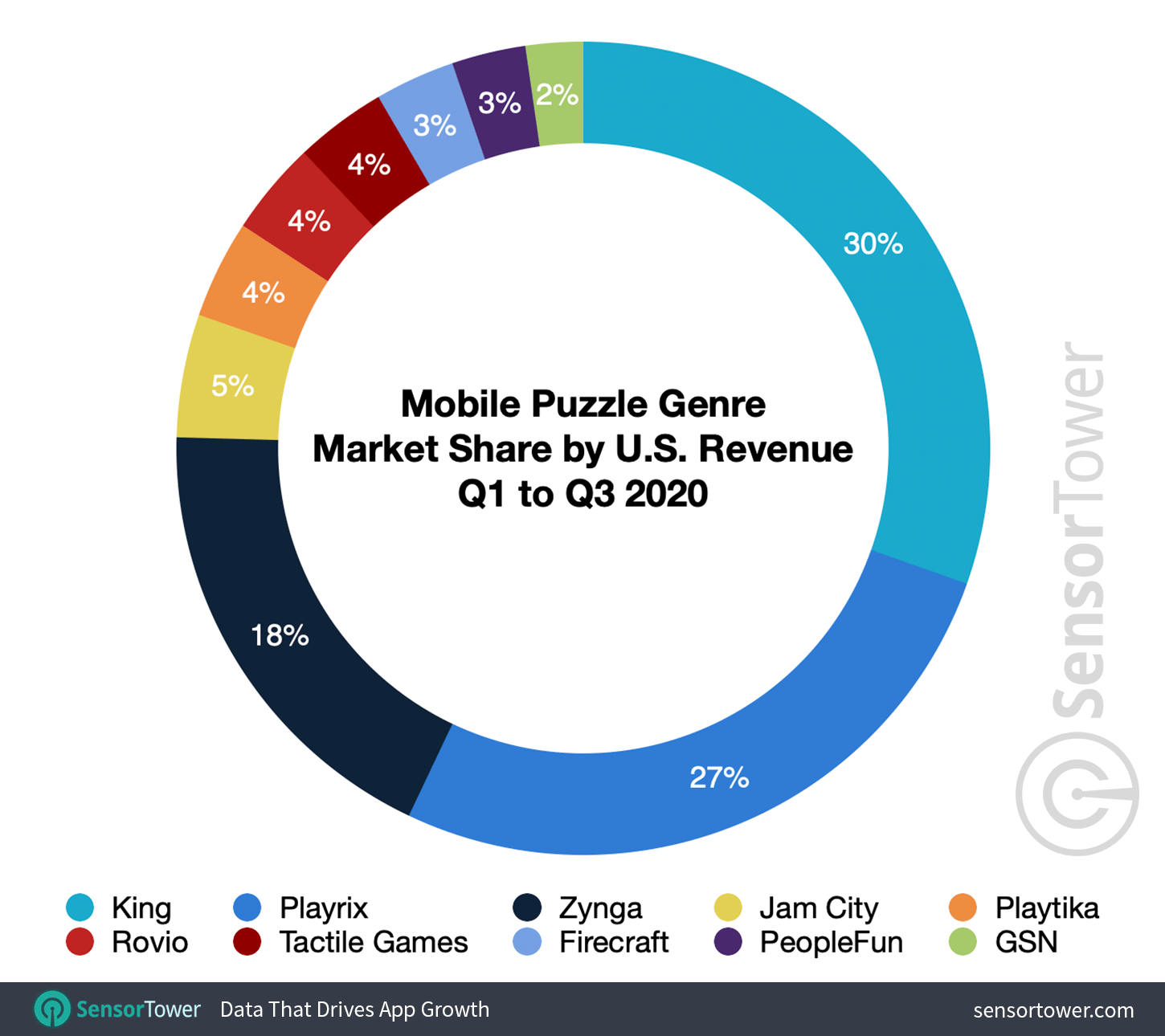

Puzzle Pieces

During the first nine months of 2020, the top publisher in the U.S. puzzle space was King—itself an Activision acquisition—with the publisher’s success in the genre powered by the eponymous Candy Crush Saga, with spending in its games up 6 percent year-over-year to approximately $846 million. Playrix’s gross revenue in the genre, meanwhile, nearly doubled Y/Y to nearly $742 million, thanks to the strong growth of its hit titles Gardenscapes, Homescapes, and Fishdom.

Zynga’s growth in the puzzle space has been boosted by its big-money acquisitions, including the recent deal for Toon Blast developer Peak Games, and the 2018 purchase of Merge Dragons studio Gram Games. If we include Peak Games revenue for the entire period of Q1 to Q3 2020, Zynga was the No. 3 publisher in the puzzle genre, generating nearly $512 million in player spending—more than double what it would have been without Peak. It’s an example of how M&A activity is being used by big publishers to cement their positions in a genre, and even become a leader in it.

Jam City ranks No. 3 for player spending, with revenue for the Cookie Jam and Panda Pop publisher buoyed by the purchase of studios such as the Disney Emoji Blitz team, while Playtika ranks No. 4 thanks to its acquisitions of the likes of Supertreat and Wooga, forming a key pillar of its strategy to be a leader in the casual games market—a mission which it is clearly making inroads on.

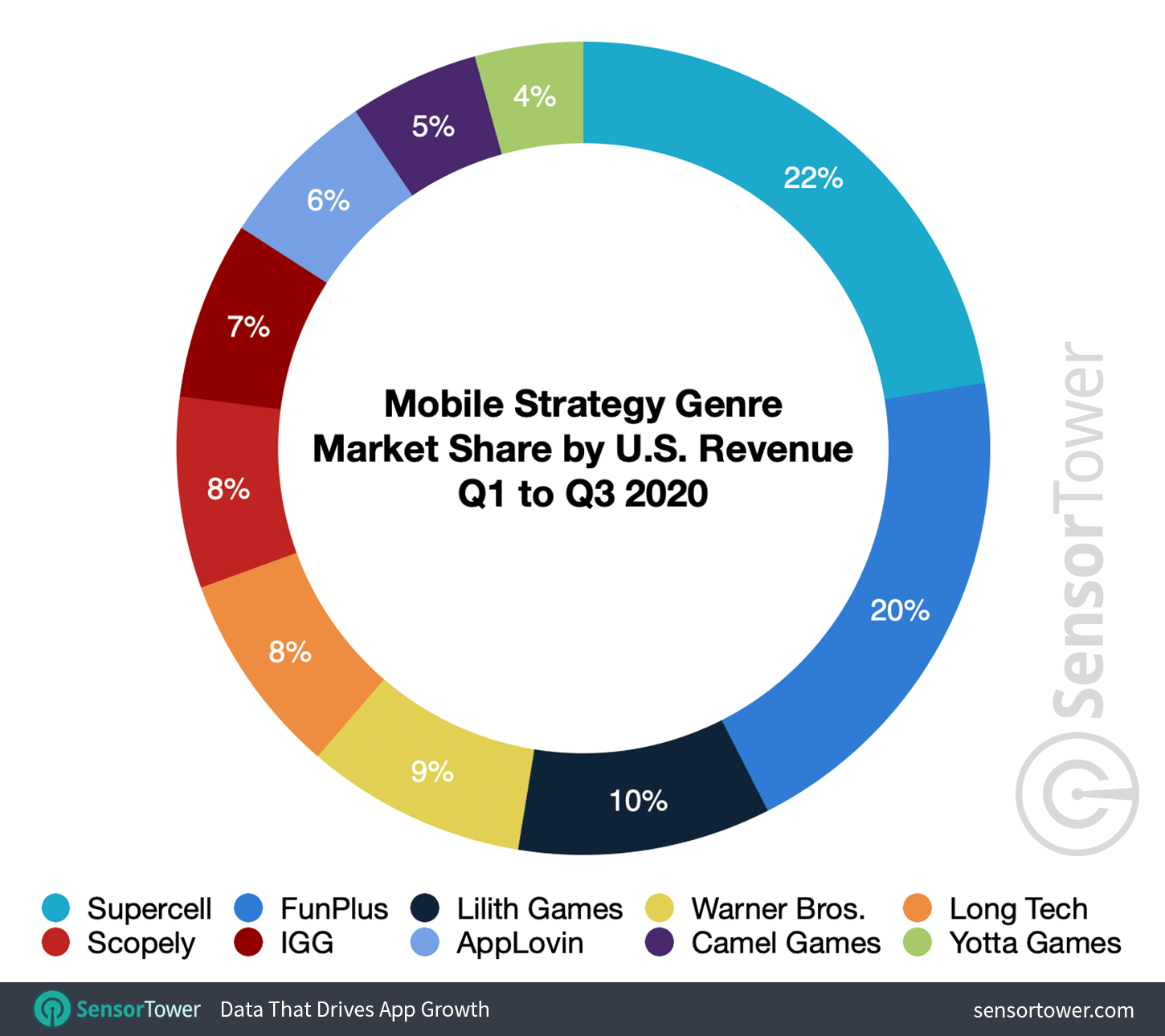

Strategy Segment

Sitting at the top of the mobile strategy games market is Clash of Clans and Clash Royale developer Supercell, which generated approximately $378 million in U.S. player spending during the first nine months of 2020. It’s followed by FunPlus at No. 2, with titles such as King of Avalon and Guns of Glory pushing the publisher’s strategy portfolio up 58.7 percent Y/Y to nearly $339 million.

Of note here is the rise of AppLovin in the genre, ranking No. 8. The publisher is best known for its casual games through Lion Studios, but in May 2020 it purchased Game of War and Final Fantasy XV: A New Empire developer Machine Zone, giving it a firm foot in the door in the strategy market. The studio’s portfolio in the genre, which it specialises in, generated U.S. player spending of approximately $108 million from Q1 to Q3 of this year and positions AppLovin in a market it had no stake in the year prior.

Scopely, meanwhile, has pushed up the rankings, having partnered with Digit Game Studios on the development of Star Trek: Fleet Command. It was a hit out of the gates, with Scopely acquiring Digit in May 2019. The deal has proven fruitful for both parties, with Fleet Command ranking as the No. 4 strategy game in the U.S. during the first nine months of 2020.

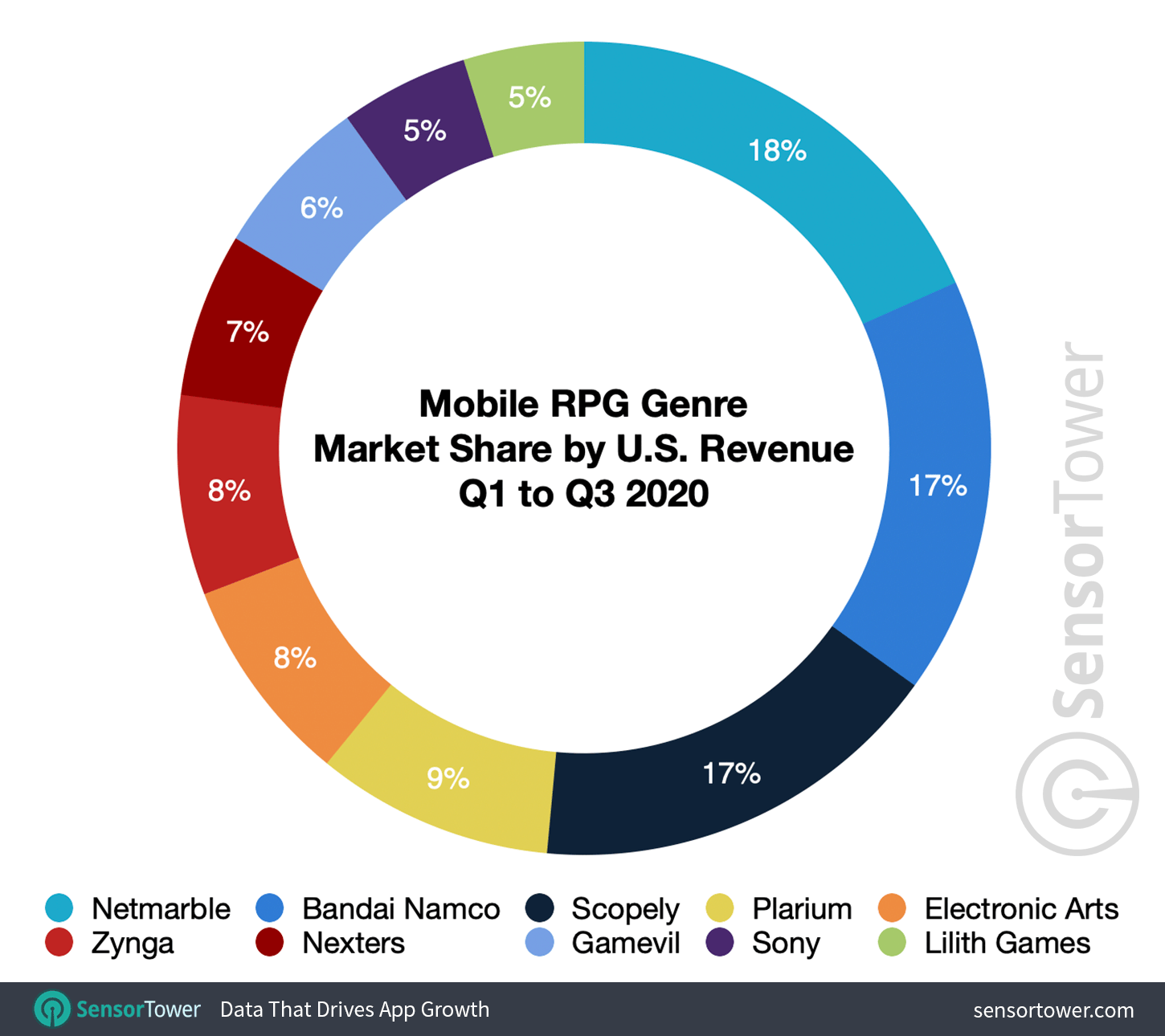

RPG Royale

Netmarble ruled the roost in the U.S. RPG market during Q1 to Q3 2020, generating more than $254 million in spending during the period, up 68.6 percent Y/Y thanks to titles including Marvel Contest of Champions from Kabam, which the South Korean publisher acquired in 2017. Bandai Namco ranked No. 2 with player spending increasing by approximately 22 percent Y/Y to more than $230 million, powered by Dragon Ball Z: Dokkan Battle and Dragon Ball Legends.

The RPG genre has witnessed a few key acquisitions over the years, with one recent key deal being that of Scopely’s purchase of FoxNext Games back in January 2020. Its flagship title, Marvel Strike Force, took in $165 million from players during the first nine months of the year in the U.S. Without that title, Scopely wouldn’t rank in the top 10 for the genre, making it an astute acquisition for the publisher. As it stands, the company ranked No. 3 for RPG revenue.

Meanwhile, casino firm Aristocrat Leisure, which has purchased Big Fish Games and Plarium in the past, ranks No. 4 for RPG revenue due to its acquisition of the latter in 2017. Zynga ranks No. 6 thanks to its decision to buy Empires & Puzzles developer Small Giant Games in 2018, with the title proving to be a huge hit.

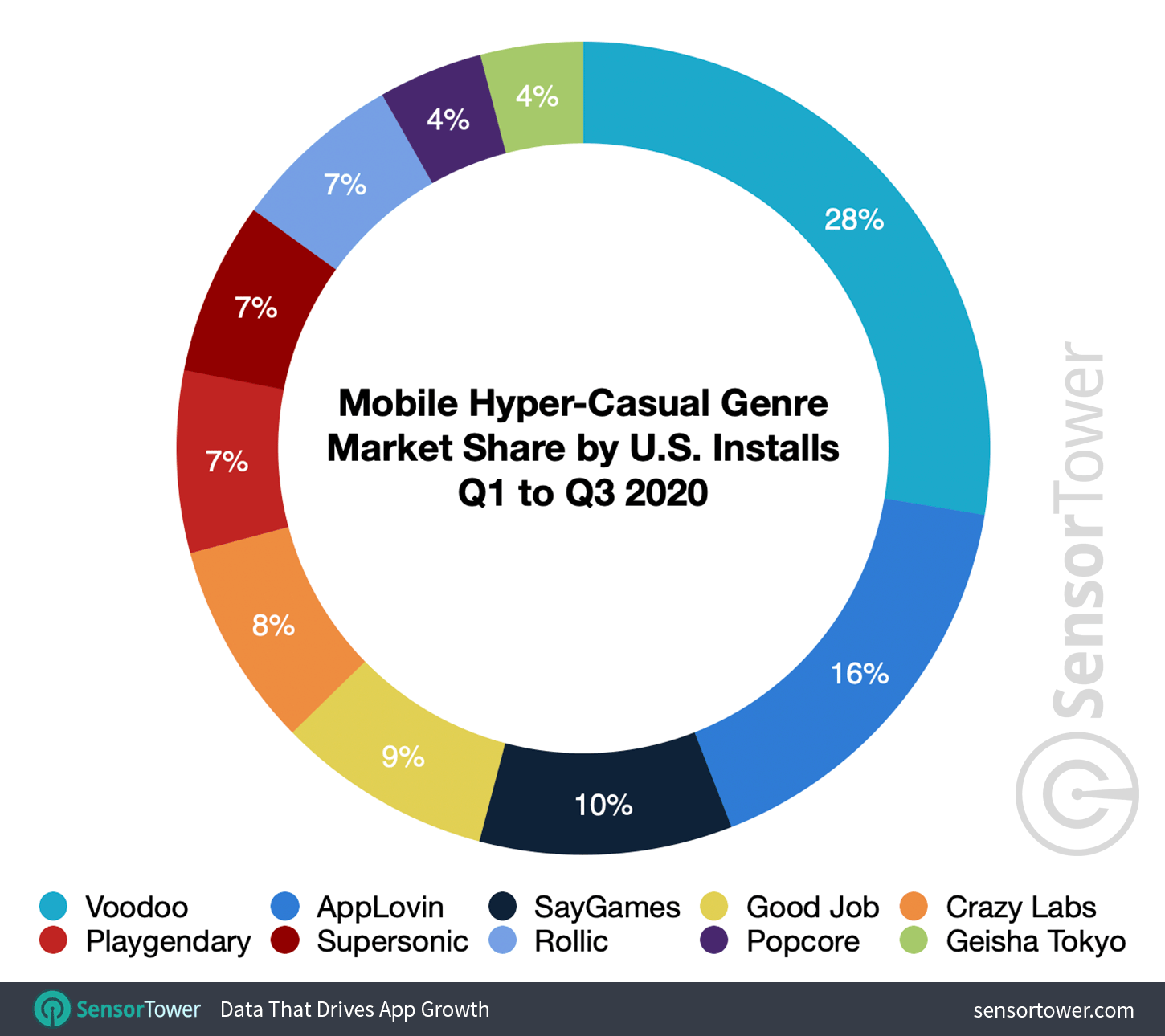

Hyper-Casual Highlights

Voodoo, which has received investment from Tencent, was the top hyper-casual games publisher between Q1 and Q3 2020, generating an estimated 210 million downloads in the U.S. during that time. AppLovin, meanwhile, which made its foray into the hyper-casual space with Lion Studios, accumulated about 125 million installs in the U.S. during the period.

The hyper-casual genre is fiercely competitive and, as such, has seen a few key entries and acquisitions. Like AppLovin, IronSource entered the space with Supersonic Studios. Zynga, meanwhile, recently acquired Rollic Games, which in the first nine months of the year would place the publisher at No. 9 for U.S. downloads in the genre.

M&A Matters

As the mobile games market continues to mature, even after more than a dozen years, it’s natural that the top publishers in the space are spending their riches on expanding their empires, while other companies outside of the mobile space are also making big investments in the world’s most lucrative games sector. The right acquisition of an established developer can propel publishers into the position of market leaders, as seen with the case of Scopely in the RPG and strategy genres and Zynga in the puzzle space. Analyzing the market share of the top players also pinpoints where some of the key innovations in the market may be happening—and where the next big acquisitions may come from.

Sensor Tower’s Store Intelligence platform is an Enterprise level offering. Interested in learning more?